Tax Time, Japan-Style

So, you’re an American living in Japan, it’s past April 15th, and your taxes are still not ready? Well, don’t worry about it quite yet. You get an automatic 2-month extension from the IRS, until June 15th, to file your income taxes. And if you want to, you can file for another extension after that, and usually you get it–but June 15th is enough, and filing for an extension would actually be more trouble than it’s worth unless you have some unfortunate and bizarre situation going on there.

Since we all get the Foreign Earned Income Exclusion (FEIE), now at $80,000 per year, most of us unlucky enough not to earn more than that end up not paying anything in taxes to the U.S.–which is fair, because we have to pay full taxes here in Japan. But we have to file with the IRS anyway.

“But I don’t owe anything, and I paid taxes to Japan, so I don’t need to file.” Well, we all wish it were so. But alas, you have to file no matter what. In fact, you have to file to get the Foreign Earned Income Exclusion–if you don’t file, then technically you will have to pay complete U.S. taxes! So make sure you do file…

In order to file, you need Form 1040, Form 2555, a 2003 “gensen chusho” form (a small slip that documents your income and tax fess for the year) from your work, and the 2003 Annual Average Rate for the yen and dollar.

By the way, here’s a news flash: As of June this year, the IRS office at the Tokyo embassy will be shutting down permanently, which sucks big-time. The person at the office said the shut-down is to save money (money that Bush has spent on Halliburton or tax breaks for billionaires). They have always been there to answer phone calls, not to mention being there to help you in person if you have problems that can’t be handled by phone. So now if you need help, you have to pay international dialing rates and wait on hold for an hour and a half to talk to someone in Philadelphia who knows nothing about paying your taxes from Japan. Ah, Bush’s America.

But if you want help in the next two months, then call (03) 3224-5466; press “8” as soon as you hear talking in order to avoid the mind-numbing voice mail handling, and instead get switched directly to an “assistor.” If they’re busy or out to lunch, then you can leave a message and they’ll get back to you.

Anyway, I decided that this year I was going to explain how to get those forms done, because there is a bit of a confusing process to go through for this (it wouldn’t be taxes if it weren’t at least a little confusing), and I tend to forget how to do this from year to year. This explanation should help all you regular Americans living in Japan do your tax returns, although:

DISCLAIMER: I am not a professional tax preparer. I do not guarantee that any of the information or advice on this page is correct. If there are any errors which lead you to make errors, that is your responsibility.

In other words, I want to try to help you, not get sued by you. So follow my advice at your own risk. that said, here we go:

(see continuation)

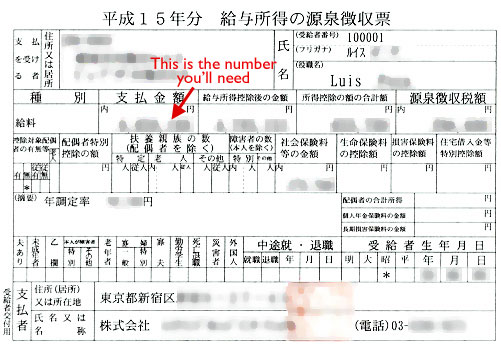

First, get your gensen choshu hyo (源泉徴収票), from the accountants at your workplace. The form looks like this:

Let’s say that the amount is 5,000,000 yen, for the sake of this example. Now go to the IRS page at the Japan embassy to find out the official exchange rate to calculate how to translate. If you trust me here, I’ll tell you now that it is 113.873. Divide your yen income by that amount; that’s your dollar income for 2003. With the example amount of 5 million yen, it comes out to $43,908.54. The Tokyo IRS office says you round to the closest dollar, so in my example it’d be $43,909. Write that number down, you’ll be using it.

Now, if you’ve paid taxes from your current address before, you’ll have gotten your 2003-1040 form book; if not, you can download the forms from the IRS at the links I showed above. The booklet, if you have it, has duplicate copies of the 1040 and 2555, which is what most people need and is what I’ll be explaining how to use.

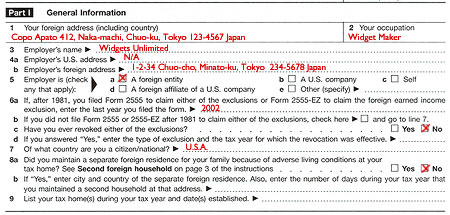

I like to start with the 2555, because there’s data from that sheet you’ll need to input early on in the 1040, and not the other way around. Start by filling out Part 1, with your name, address, and other info.

Don’t forget your Social Security number at the top. Fill out your address and occupation, and the name and address of your employer. Ask your employer for this, because they may have a special business address for you to use. If you have filed a 2555 before, write the year you did so on 6a. It is likely that you’ll check the “no” box on 6c and 8a, but check them and make sure anyway. On line 7, put your country of citizenship.

Now you choose which way you’ll prove that you lived outside the U.S. There’s the “Bona-Fide” test, and then there’s the “Physical Presence” test. The bona-fide test is if you (a) have lived in Japan for more than one year, and (b) have a contract period longer than one year. Since most foreign workers in Japan are limited to one-year renewable contracts, the physical presence test is called for; you can skip over Part II and go straight to Part III on page 2.

I’ve been doing the Physical Presence test every time since I came to Japan, and I just got misdirected into doing the bona-fide test by the IRS office. Yesterday, I told them I was doing the physical presence test, and the woman acted like I was crazy, the bona-fide test is much easier! I asked her if she was sure I qualified; she asked if I’d lived in Japan for more than one year, and when I said “yes,” she told me that I should really do the bona-fide. So I spent much of last night and this morning trying to figure it out, and trying many times to call the office to clear up subtle questions. When I finally got through to the IRS office (a lot of we’re-busy-now hang-ups)–I think I got the same woman–I asked, among other things, about line 15a and what the contract terms were about, and she said that if my contract was for one year or less I wouldn’t qualify, and would have to do the physical presence test. When I complained that yesterday she had directed me without any reservation to doing the bona-fide, she shot back, “well, maybe you didn’t tell me you had a one year contract!” Yeah, lady. Thanks a lot for nothing. Good thing I worked on copies and didn’t mark up my originals.

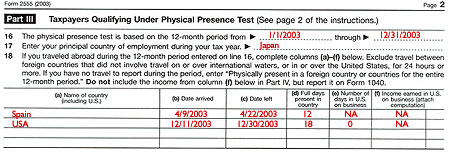

Next, if you traveled in 2003, get out your passport and figure out departure and arrival dates, and note which countries you visited on each trip; that’ll be needed for the 2555. In my case, I visited Spain in April and the U.S. in December.

With this information, I can fill out the physical presence section:

Note that you only have to count the full days, days in which you are present in another country from start to finish; therefore, my Spain trip counts as 12 days, and my American trip as 18. That brings me to a total of 30–which is good, because if it is more than 35, then I have to go to some trouble to offset the one-year physical test period, and that entails more confusion.

From here, things get a bit more straightforward. On page 2, just fill in your dollar income, the same number, on lines 19, 24 and 26. You would only need to fill out other stuff if you have special financial conditions, like special reimbursements for housing, cars, meals, home leave, etc. which is not included in your income total stated in your gensen choshu hyo. Again, most people don’t have this–if you do, you’ll have to translate the amount into yen and add it to the total.

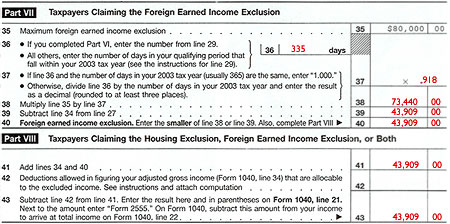

Then you carry your total–still my imaginary $43,909 in my case–to line 27 on page 3, the last page. You should check “no” under line 27 unless you want to claim the housing deduction–not necessary if your total will be under $80,000. So we jump to Part VII.

On line 36, I write down how many days I was in Japan–365 minus the number of full days counted in Part III, Line 18. In my case, 30 full days, making my amount for line 36 “335.” Then you have to divide your number from line 36 by 365, which in my case is .918, and put that on line 37. Then multiply line 37 by $80,000. I get $73,440. That’s the largest amount I can deduct. But since my total income was $43,909, I put that number on lines 39 and 40–on line 40 because it’s the smaller number.

The same amount is carried to lines 41 and 43, so long as you have no special deductions–and you’re done with Form 2555!

Now go to your 1040 form. Fill out your name, address and other personal information, as well as your filing status and exemptions (for me, just the “yourself” exemption).

Next, on line 7, put your income in dollars. Above the dotted line to the left of the number you just wrote, pen in the calculation that got that number–e.g., “¥5,000,000 ÷ 113.873 = $43,909.”

![]()

Next, you have to add any interest or dividend income from the U.S. For example, if you have a bank account, then you should have a 1099-INT form that was sent to you from your bank listing the total interest income for 2003. If you have stock and received dividends, that must be listed also. Any taxable income of that sort has to be included here. If you do not have that information available, then there is a solution: I do not in any way comment on its legality, but you could possibly enter an amount that you are certain is greater than the amount you actually earned. Say you have a few thousand dollars in the bank at home–the interest you got was surely not more than $100. And since that is way under the minimum tax level, you could write $100.00 on the form. Whatever your number is, write that in on line 8a.

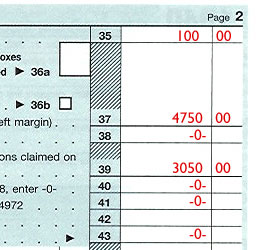

Then, on line 21, write “FORM 2555” in the blank white box in the blue zone, and write the amount of your income, from line 43 of Form 2555, in brackets (denoting a negative amount) in the number area of line 21. On line 22, you add up all the numbers, which should be the amount from 8a, as lines 7 and 21 cancel each other out. In my imaginary case here, it is $100. Since I have no special adjustments, I simply bring the total down to line 34, and then to page 2 on line 35.

On line 37, fill in 4,750 (the single-or-married-filing-separately deduction, unless you are filing married jointly). You can subtract that amount from your total on line 35, so the total will clearly be “0”. On line 39, you get to deduct another $3,050 for each exemption claimed on page 1 line 6, which for me is just one, but it is moot as my amount is already zero and anything deducted will still add up to zero. And from there, it’s zeroes all the way down to line 72, the amount you owe.

Sign it, seal it, and send it off.

I usually like to take it to the embassy myself, often because there’s other stuff I can do there and it’s not far from my work. This year I want to pick up voter registration materials, so I’ll be going in early next week.

I hope this was of some help!

Even if you made MORE than the $80,000 FEIE, there’s still a good chance you don’t owe taxes. You also get credit for any foreign taxes you paid on income over that amount; for housing; for dependents (but only if they have a SSN or a special tax no. you can get from the US gov’t. In other words, you can’t count your foreign spouse unless you have one of these numbers. But beware! That also means your foreign spouse’s income is liable for US Taxes! Yup! The long arm of the IRS.)

That and all sorts of info are included in IRS Pub. 54

http://www.irs.gov/newsroom/article/0,,id=108276,00.html

But how much in Japanese taxes did you pay? It’s best to ask someone at your company to explain the form and how it’s calculated; or you can wade thru these exciting documents from the Ministry of Finance:

http://www.mof.go.jp/english/tax/taxes2003e.htm

And hey! Haven’t filed in a while? Amnesty is available, or at least was last time I checked. Best call the US Embassy for details. There’s a specific bit of info you have to write on the top of your form.

wow. you are awesome.

i pecked around the internet back on april 14th and downloaded the forms and found out about that 2 month extension and then i did….

nothing.

i guess i was waiting around to stumble upon this step by step. thanks a million.

I have learned all of this…. and have been explaining it to all of my friends here one by one. It is nice to see somebody else has done it (and with a pleasant writing style!)

Thank you!

Mickey

Hello fellow JETs!

I was an ALT from the States last year, (Aug 2005 – Aug 2006), but I left after that first year. Before I left, I was given that little blue booklet that still needs to be sent somewere in Japan to retrieve my tax return. Can someone please help me through this? The only other JET in my small town was a CIR, who files differently. I got through the whole American tax season alright, (thank you by the way), but I would like to collect my check from Japan sometime soon and have no idea how.

Hoping to hear from you all!

Jessica

Kansas City, Missouri

I can’t, sorry… can anyone else?

This post was very helpful…thanks.

If your total in savings and investment accounts in Japan exceeds $10000 I believe you need to file 1040 Sch B (line 7-8) and Treasury Dept for TD F 90-22.1 (available at the IRS website) also. Ask the IRS or a tax expert to confirm…I’m not an expert either.